注意

转到末尾 下载完整示例代码。

3.1.6.8. 9/11 前后的机票价格¶

这是一个类似商业智能 (BI) 的应用程序。

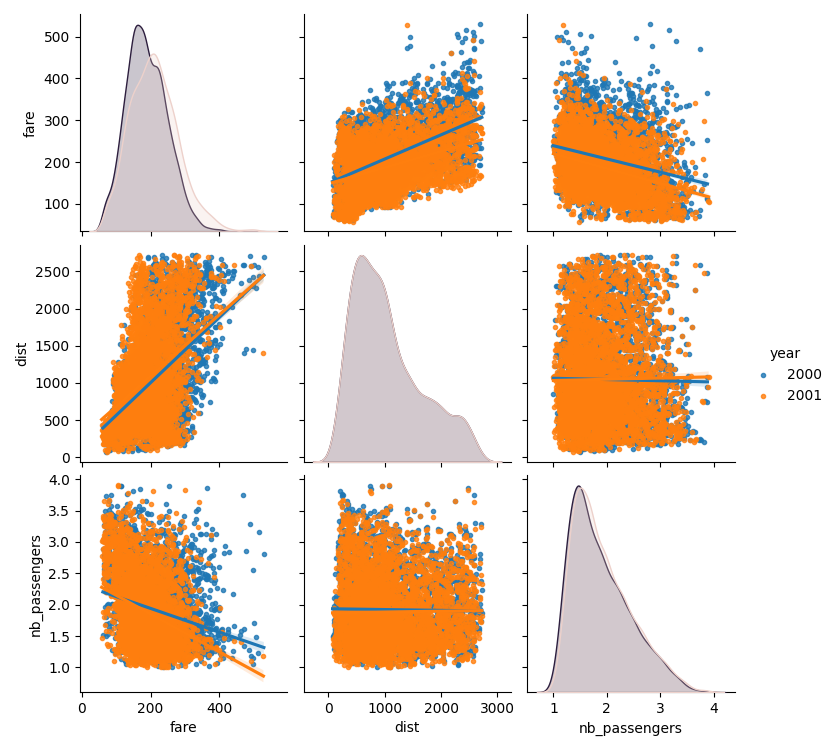

有趣的是,我们可能希望研究机票价格随年份的变化,并根据行程进行配对,或者忽略年份,只作为行程终点的函数。

使用 statsmodels 的线性模型,我们发现,无论是使用 OLS(普通最小二乘)还是稳健拟合,截距和斜率都显著不为零:机票价格在 2000 年至 2001 年间下降,并且它们对行程距离的依赖性也下降了

# Standard library imports

import os

加载数据

import pandas

import requests

if not os.path.exists("airfares.txt"):

# Download the file if it is not present

r = requests.get(

"https://users.stat.ufl.edu/~winner/data/airq4.dat",

verify=False, # Wouldn't normally do this, but this site's certificate

# is not yet distributed

)

with open("airfares.txt", "wb") as f:

f.write(r.content)

# As a separator, ' +' is a regular expression that means 'one of more

# space'

data = pandas.read_csv(

"airfares.txt",

delim_whitespace=True,

header=0,

names=[

"city1",

"city2",

"pop1",

"pop2",

"dist",

"fare_2000",

"nb_passengers_2000",

"fare_2001",

"nb_passengers_2001",

],

)

# we log-transform the number of passengers

import numpy as np

data["nb_passengers_2000"] = np.log10(data["nb_passengers_2000"])

data["nb_passengers_2001"] = np.log10(data["nb_passengers_2001"])

/home/runner/work/scientific-python-lectures/scientific-python-lectures/packages/statistics/examples/plot_airfare.py:38: FutureWarning: The 'delim_whitespace' keyword in pd.read_csv is deprecated and will be removed in a future version. Use ``sep='\s+'`` instead

data = pandas.read_csv(

创建一个以年份为属性的数据帧,而不是单独的列

# This involves a small danse in which we separate the dataframes in 2,

# one for year 2000, and one for 2001, before concatenating again.

# Make an index of each flight

data_flat = data.reset_index()

data_2000 = data_flat[

["city1", "city2", "pop1", "pop2", "dist", "fare_2000", "nb_passengers_2000"]

]

# Rename the columns

data_2000.columns = pandas.Index(

["city1", "city2", "pop1", "pop2", "dist", "fare", "nb_passengers"]

)

# Add a column with the year

data_2000.insert(0, "year", 2000)

data_2001 = data_flat[

["city1", "city2", "pop1", "pop2", "dist", "fare_2001", "nb_passengers_2001"]

]

# Rename the columns

data_2001.columns = pandas.Index(

["city1", "city2", "pop1", "pop2", "dist", "fare", "nb_passengers"]

)

# Add a column with the year

data_2001.insert(0, "year", 2001)

data_flat = pandas.concat([data_2000, data_2001])

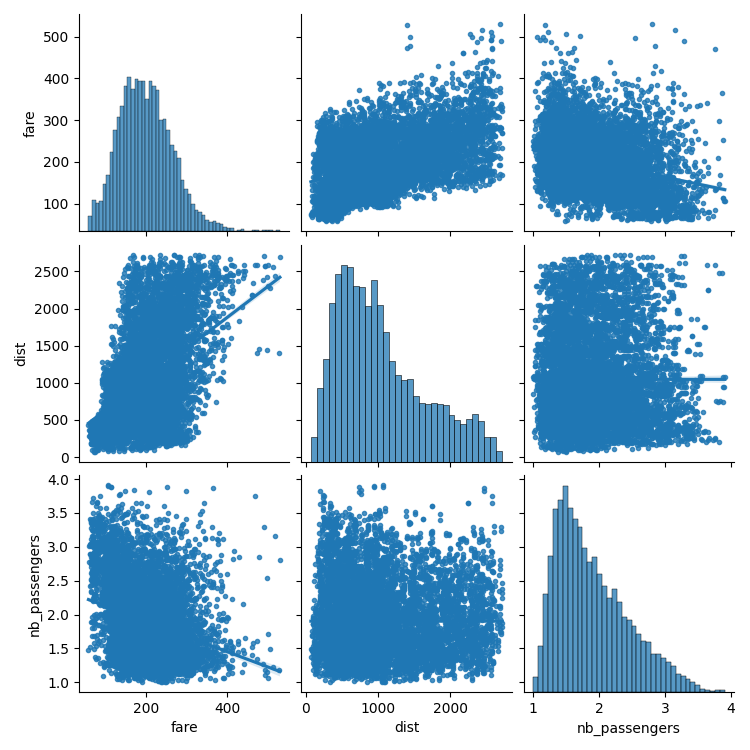

绘制散点矩阵,突出显示不同的方面

import seaborn

seaborn.pairplot(

data_flat, vars=["fare", "dist", "nb_passengers"], kind="reg", markers="."

)

# A second plot, to show the effect of the year (ie the 9/11 effect)

seaborn.pairplot(

data_flat,

vars=["fare", "dist", "nb_passengers"],

kind="reg",

hue="year",

markers=".",

)

<seaborn.axisgrid.PairGrid object at 0x7f78e5312f30>

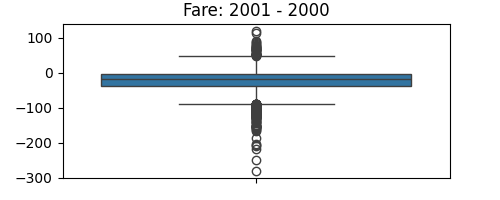

绘制机票价格差异

import matplotlib.pyplot as plt

plt.figure(figsize=(5, 2))

seaborn.boxplot(data.fare_2001 - data.fare_2000)

plt.title("Fare: 2001 - 2000")

plt.subplots_adjust()

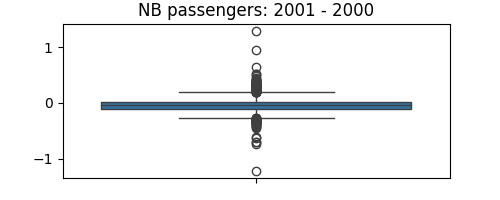

plt.figure(figsize=(5, 2))

seaborn.boxplot(data.nb_passengers_2001 - data.nb_passengers_2000)

plt.title("NB passengers: 2001 - 2000")

plt.subplots_adjust()

统计检验:机票价格对距离和乘客数量的依赖性

OLS Regression Results

==============================================================================

Dep. Variable: fare R-squared: 0.275

Model: OLS Adj. R-squared: 0.275

Method: Least Squares F-statistic: 1585.

Date: Mon, 07 Oct 2024 Prob (F-statistic): 0.00

Time: 04:57:10 Log-Likelihood: -45532.

No. Observations: 8352 AIC: 9.107e+04

Df Residuals: 8349 BIC: 9.109e+04

Df Model: 2

Covariance Type: nonrobust

=================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------

Intercept 211.2428 2.466 85.669 0.000 206.409 216.076

dist 0.0484 0.001 48.149 0.000 0.046 0.050

nb_passengers -32.8925 1.127 -29.191 0.000 -35.101 -30.684

==============================================================================

Omnibus: 604.051 Durbin-Watson: 1.446

Prob(Omnibus): 0.000 Jarque-Bera (JB): 740.733

Skew: 0.710 Prob(JB): 1.42e-161

Kurtosis: 3.338 Cond. No. 5.23e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 5.23e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

Robust linear Model Regression Results

==============================================================================

Dep. Variable: fare No. Observations: 8352

Model: RLM Df Residuals: 8349

Method: IRLS Df Model: 2

Norm: HuberT

Scale Est.: mad

Cov Type: H1

Date: Mon, 07 Oct 2024

Time: 04:57:10

No. Iterations: 12

=================================================================================

coef std err z P>|z| [0.025 0.975]

---------------------------------------------------------------------------------

Intercept 215.0848 2.448 87.856 0.000 210.287 219.883

dist 0.0460 0.001 46.166 0.000 0.044 0.048

nb_passengers -35.2686 1.119 -31.526 0.000 -37.461 -33.076

=================================================================================

If the model instance has been used for another fit with different fit parameters, then the fit options might not be the correct ones anymore .

统计检验:机票价格对距离的回归:2001/2000 的差异

OLS Regression Results

==============================================================================

Dep. Variable: fare_2001 R-squared: 0.159

Model: OLS Adj. R-squared: 0.159

Method: Least Squares F-statistic: 791.7

Date: Mon, 07 Oct 2024 Prob (F-statistic): 1.20e-159

Time: 04:57:10 Log-Likelihood: -22640.

No. Observations: 4176 AIC: 4.528e+04

Df Residuals: 4174 BIC: 4.530e+04

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 148.0279 1.673 88.480 0.000 144.748 151.308

dist 0.0388 0.001 28.136 0.000 0.036 0.041

==============================================================================

Omnibus: 136.558 Durbin-Watson: 1.544

Prob(Omnibus): 0.000 Jarque-Bera (JB): 149.624

Skew: 0.462 Prob(JB): 3.23e-33

Kurtosis: 2.920 Cond. No. 2.40e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 2.4e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

脚本的总运行时间:(0 分钟 7.694 秒)